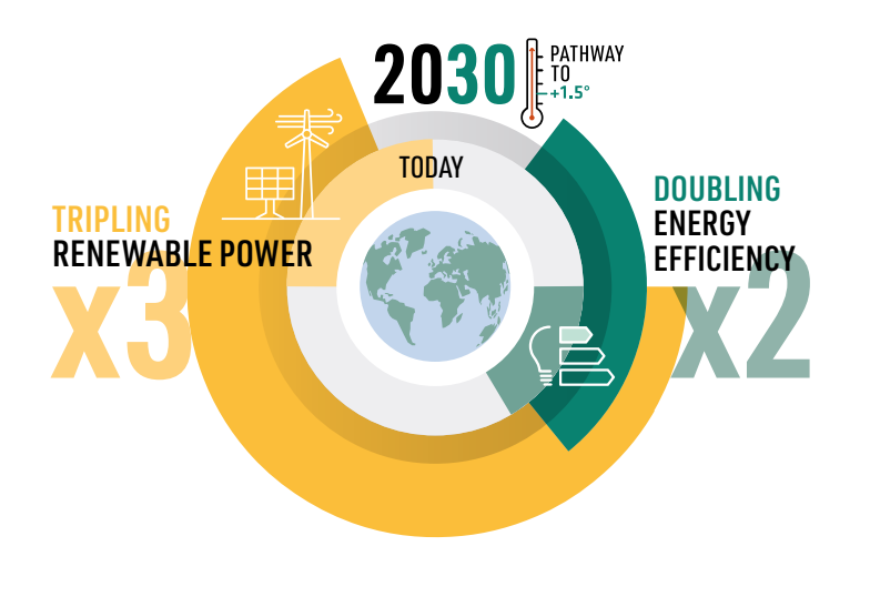

Tripling renewable power and doubling energy efficiency by 2030: Crucial steps towards 1.5°C

KEY RECOMMENDATIONS

TOTAL GLOBAL RENEWABLE POWER GENERATION CAPACITY WILL NEED TO TRIPLE BY 2030 to reach more than 11 000 GW under IRENA’s 1.5°C Scenario in the World Energy Transitions Outlook, with solar photovoltaic (PV) and wind power accounting for about 90% of renewable energy capacity additions.

ENERGY EFFICIENCY IMPROVEMENTS MUST DOUBLE BY 2030 TO REMAIN ON A 1.5°C PATHWAY. In IRENA’s 1.5°C Scenario this will be driven by a combination of efficient technologies in end-use sectors and extensive electrification. These vital milestones must be achieved to keep the global energy transition on track to meet Paris Agreement goals.

A COMPREHENSIVE MIX OF POLICIES IS NEEDED TO ACHIEVE THESE AMBITIOUS TARGETS. Aside from deployment and enabling policies, structural change is needed to ensure the transition to an energy-efficient economy and a renewables-based power system is just and fair, and provides benefits for all.

ENERGY EFFICIENCY POLICY MEASURES should include: the adoption of targets with specific time horizons; strong regulatory frameworks including building codes and energy efficiency standards for appliances; fiscal and financial incentives; and public campaigns to build awareness of the role of energy efficiency measures, public transport and green mobility for cost savings and collective decarbonisation goals.

RENEWABLE ENERGY DEPLOYMENT REQUIRES ENABLING MEASURES THAT GO BEYOND REGULATIONS OR FISCAL AND FINANCIAL INCENTIVES. The organisational structures of power sectors must be reshaped to integrate a higher share of renewables. Procurement mechanisms must be designed in a way that strengthens value chains and trade, and industrial policies must be fit for building resilient supply chains. Education, training, re-skilling and up-skilling should be prioritised; women and under-represented groups must be empowered; and collaboration between industry, civil society, policy makers and other key stakeholders should be encouraged.

EXISTING ELECTRICITY INFRASTRUCTURE SHOULD BE EXPANDED AND MODERNISED TO CREATE A NEW ENERGY SYSTEM FIT FOR RENEWABLES. There is an urgent need to boost crosssector infrastructure planning, increase cross-border co-operation and develop regional power grids. Action is also needed to drive grid modernisation and expansion and ensure supply-side flexibility and demand-side management.

RENEWABLE POWER CAPACITY SHOULD BE INCREASED MORE RAPIDLY IN DEVELOPING COUNTRIES, given their growing electricity demand and the important role of renewables in addressing the significant energy access deficit in these countries.

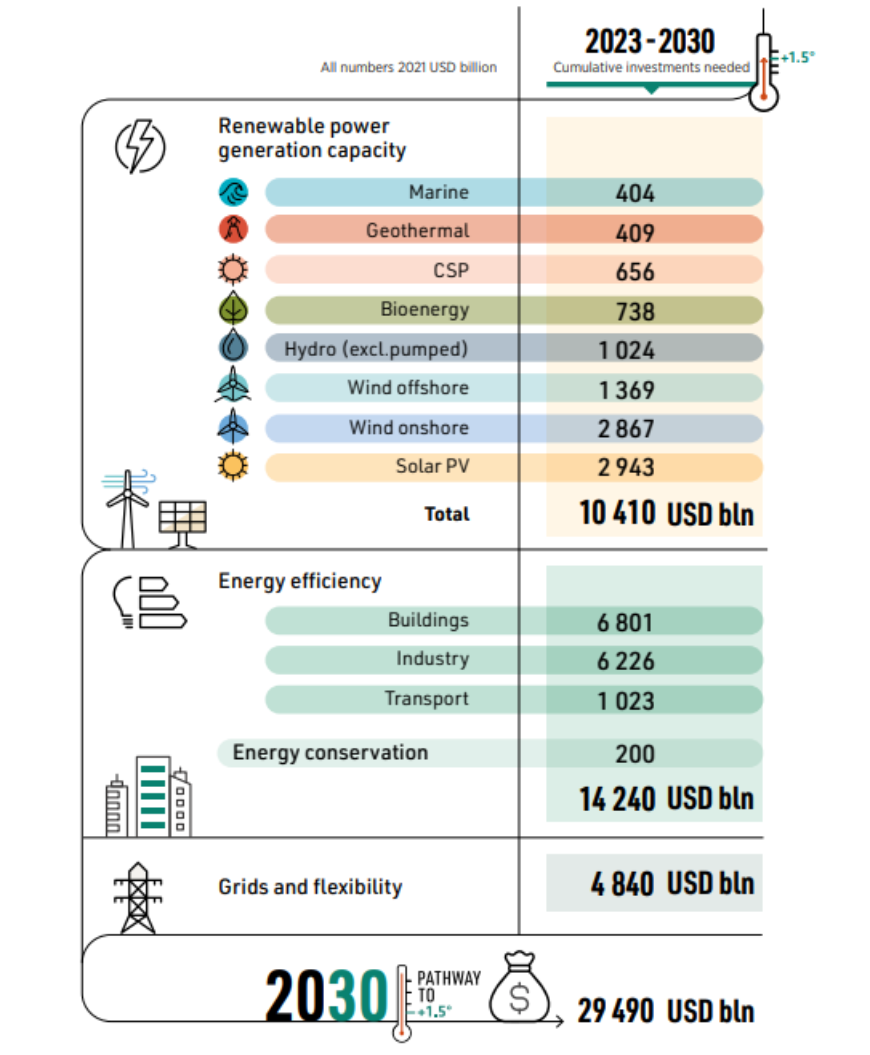

WE MUST RAPIDLY MOBILISE PUBLIC AND PRIVATE FINANCE TO TRIPLE RENEWABLE POWER CAPACITY AND DOUBLE ENERGY EFFICIENCY. Annual average investment in renewable power generation must reach USD 1 300 billion by 2030, compared to 486 billion in 2022. In the developing world, we must minimise investment risks and provide access to low-cost financing. The global financial architecture must be reformed to support the energy transition in the Global South. Climate-related funding from multilateral development banks must be ramped up, and public capital should be redirected from the fossil fuels sector to renewable energy.

THIS WILL REQUIRE STRONG INTERNATIONAL COLLABORATION. Immediate efforts are required to facilitate and contribute to multilateral initiatives that promote knowledge sharing and capacity building to deliver a just transition whilst also safeguarding nature and biodiversity. Collaboration is urgently required to foster collective action on governance, climate finance and innovation. North-South and South-South dialogues should be cultivated; groups like the G7 and G20 must mobilise support and investment; and just transition funds should be established and operationalised in emerging economies.

INTRODUCTION

The United Nations Intergovernmental Panel on Climate Change (IPCC), in its latest Assessment Report (AR6), sent a clear message to the world that this decade is critical to our success in limiting global surface temperature increase to 1.5°C above pre-industrial levels by the end of this century (IPCC, 2023). There is an urgent need for rapid and immediate action to reduce global net anthropogenic carbon dioxide (CO2) emissions by almost 50% from 2019 levels by 2030, with a significant proportion of this reduction occurring within the field of energy.

However, the energy transition remains off-track and global greenhouse gas emissions have reached record levels. IRENA’s flagship report, World Energy Transitions Outlook 2023: 1.5°C pathway, shows that even if current pledges and plans made by national governments – including Nationally Determined Contributions (NDCs), long-term low greenhouse gas emission development strategies (LT-LEDS) and other commitments – are fully implemented, this would serve to reduce CO2 emissions by only 6% in 2030 compared to 2022 levels. This is far below the emission reductions required to place the world on a 1.5°C pathway. The message is clear: we cannot limit global surface temperature increase to 1.5°C above pre-industrial levels by the end of this century without rapid, sustained and concerted action.

COP28 marks the year of the first Global Stocktake (GST), through which policy makers, industry, financial institutions, civil society and other stakeholders will reflect on the progress achieved in implementing climate pledges since the adoption of the Paris Agreement in 2015. The World Energy Transitions Outlook 2023 concludes that a significant acceleration in the deployment of renewable energy, energy storage and renewable fuels, coupled with tangible progress in energy efficiency and electrification of end-use sectors, are required to put the world back on track in this decade to meet global climate goals (IRENA, 2023a). 1

The global energy transition requires a significant reduction in carbon emissions across the entire energy industry, as well as in end-use sectors. Leveraging low-cost solar PV, onshore and offshore wind, and other renewable electricity generation sources, the power sector must lead the way as solutions in other sectors scale up. Accelerating the progress of the transition worldwide requires a holistic approach, backed by systemic innovation to transform existing structures and systems built for the fossil fuel era.

Whilst the phase down of fossil fuels is both essential and inevitable, it must also be responsible. The transition needs to be delivered in a way that ensures energy security, accessibility and affordability, while also sustaining socio-economic development and adopting nature-positive approaches. The speed at which the transition is achieved will be determined by how quickly zero-carbon alternatives can be introduced and scaled up.

Greater ambition and stronger collective action are immediately required to accelerate progress, particularly in renewable energy and energy efficiency. Against this backdrop, policy makers, energy authorities, industry and civil society have an opportunity to align at COP28 to agree global targets to triple renewable power generation capacity and double the energy efficiency improvement rate by 2030. These goals represent some of the most important levers for change to advance the energy transition this decade.

This report consolidates high-level analysis of these targets, detailing existing shortfalls and identifying key enablers to resolve them. It represents global perspectives within the renewable energy and climate change space, with the COP28 Presidency, the International Renewable Energy Agency (IRENA) and the Global Renewables Alliance (GRA) uniting to provide concrete recommendations on the means to meet these renewable power and energy efficiency targets.

The solutions presented are technologically mature, cost-competitive and commercially available, and can be scaled up rapidly in most countries around the world; indeed, utility-scale solar PV and onshore wind are already the most cost-competitive sources of new electricity supply in most countries today (IRENA, 2023b). Accelerating progress in renewable energy deployment and energy efficiency improvement measures this decade would contribute to a cleaner energy system, improve energy security and reduce exposure – both in industry and for consumers – to the damaging risks of highly volatile fossil fuel prices. It would also improve air quality and reduce health costs; deliver universal access to clean affordable energy; and provide greater collective security and well-being. With the right policies in place, the global energy transition will also bring extensive socio-economic benefits, including in the form of job creation and income generation.

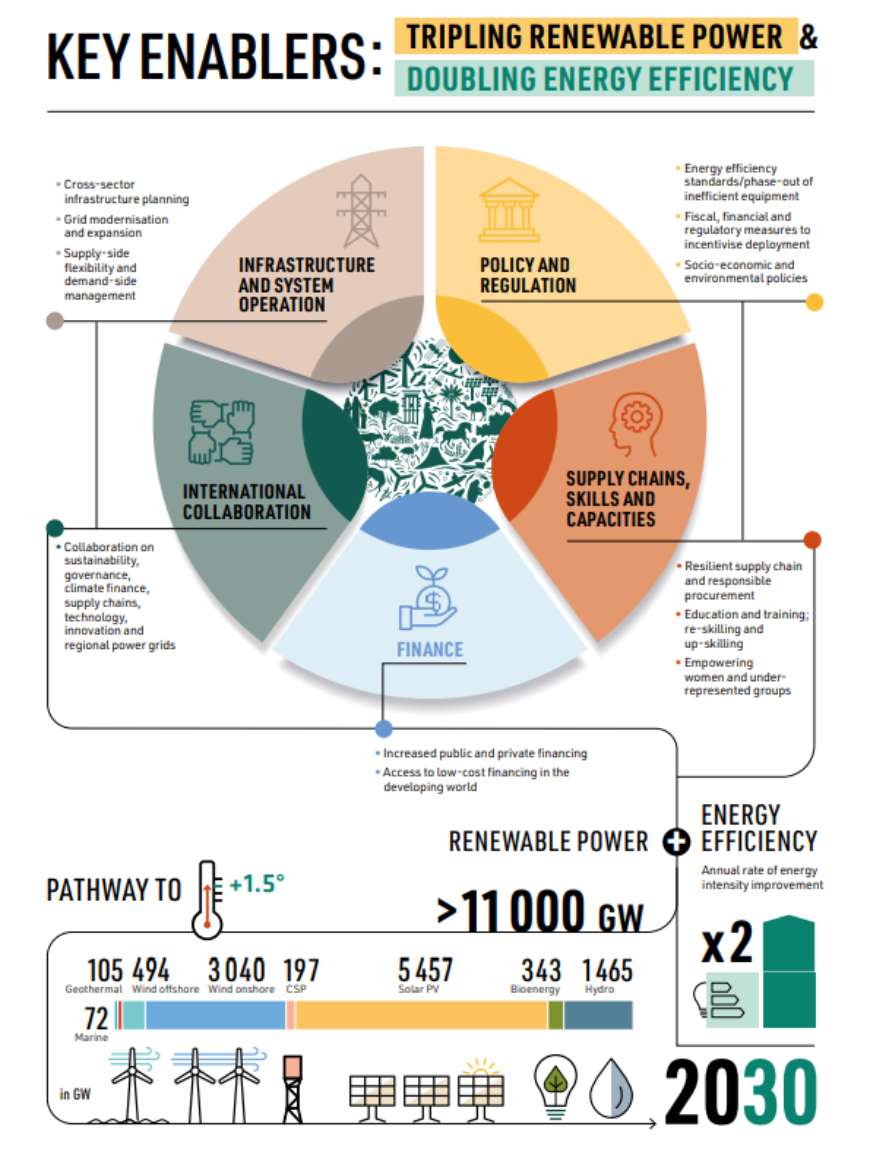

The key enabling frameworks, policies and recommendations detailed in this report provide concrete advice to governments around the world on the necessary steps required between now and 2030 to meet these targets. Realising the targets, in accordance with IRENA’s 1.5°C Scenario, would require a cumulative global installed renewable electricity generation capacity of over 11 000 GW, and a doubling of the annual energy efficiency improvement rate from the current level by 2030 (IRENA, 2023a).

It is essential that global leaders convening at COP28 demonstrate the collective will to set a new pace for action this decade by committing to these targets; in short, this is a critical step in a critical decade to keep the 1.5°C target within reach. This will require accelerated actions in many areas, in particular modernising and expanding physical energy infrastructure; improving power system operations; establishing the right policies and regulatory frameworks; building resilient supply chains; and developing skills and institutional capacities. These actions must be underpinned by a significant increase in public and private financing, particularly to support the developing world.

To ensure the energy transition is both just and inclusive, greater international collaboration is also needed. Worldwide, around 675 million people still lack access to electricity and 2.3 billion lack access to clean cooking methods (IEA et al., 2023). Providing renewable energy to those populations would contribute significantly to achieving Sustainable Development Goal 7 to Ensure access to affordable, reliable, sustainable and modern energy for all.

Forewords

Dr Sultan Al Jaber

|

|

Francesco La Camera

|

|

Bruce Douglas

|

|

Preface

Since the Rio Earth Summit and the adoption of the United Nations Framework Convention on Climate Change (UNFCCC) in 1992, the Conference of the Parties to the Convention (COP) has convened signatory Parties each year to determine ambitions and responsibilities, and identify and assess the progress of climate measures. The 21st session of the COP (COP21) led to the Paris Agreement, which mobilised collective action to limit the increase in global average temperature to well below 2°C above pre-industrial levels, pursue efforts to limit the temperature increase to 1.5°C above pre-industrial levels, and strengthen the global response to the threat of climate change.

COP28, and the first Global Stocktake of the Paris Agreement, can be the turning point on climate action over this critical decade to accelerate a transition that puts economies on the path toward a new low-carbon, high-growth, sustainable economic model in a way that is both transformational and just. COP28 has the vision to deliver on the pillars of the Paris Agreement, focusing on specific action on four paradigm shifts:

- fast-tracking the energy transition and slashing emissions before 2030;

- transforming climate finance, by delivering on old promises and setting the framework for a new deal on finance;

- putting nature, people, lives and livelihoods at the heart of climate action; and

- mobilising for the most inclusive COP ever.

Disclaimer and acknowledgements

This publication and the material herein are provided “as is”. All reasonable precautions have been taken by the copyright holders to verify the reliability of the material in this publication. However, neither the COP28 Presidency, IRENA, GRA, nor any of their officials, agents, data or other thirdparty content providers provides a warranty of any kind, either expressed or implied, and they accept no responsibility or liability for any consequence of use of the publication or material herein. The information contained herein does not necessarily represent the views of all Members of IRENA or the GRA and its constituent associations. The mention of specific companies or certain projects or products does not imply that they are endorsed or recommended by the COP28 Presidency, IRENA or the GRA in preference to others of a similar nature that are not mentioned. The designations employed and the presentation of material herein do not imply the expression of any opinion on the part of the COP 28 Presidency, IRENA or the GRA concerning the legal status of any region, country, territory, city or area or of its authorities, or concerning the delimitation of frontiers or boundaries.

Acknowledgements

This report is the result of a collaboration between the COP28 Presidency, the International Renewable Energy Agency and the Global Renewables Alliance. The report draws extensively on the analysis presented in IRENA’s World Energy Transitions Outlook 2023: 1.5°C pathway and several other IRENA reports, complemented by various reports published by the members of the GRA.

The report was co-ordinated and compiled by: Francis Field, Ute Collier, Ricardo Gorini, Yong Chen, Diala Hawila, Michael Taylor and Faran Rana (IRENA); Joyce Lee and Reshmi Ladwa (GWEC); Bruce Douglas and Beniamin Strzelecki (GRA); and Harley Higgins Watson and Yasin Kasirga (COP28).

Valuable inputs and review were provided by Roland Roesch, Rabia Ferroukhi, Elizabeth Press, Nicholas Wagner, Mengzhu Xiao, Sean Collins, Stuti Piya, Gerardo Escamilla, Rodrigo Leme, Fransisco Boshell, Arina Anisie, Gayathri Prakash, Isaline Court, Ilina Radoslavova Stefanova and Paul Komor (IRENA); Adnan Z. Amin (COP28); Ben Backwell (GWEC); Trigya Singh (GRA); Julia Souder, Alex Campbell and Gabe Murtaugh (Long-Duration Energy Storage Council); Máté Heisz, Abdallah Alshamali and Alyssa Pek (Global Solar Council); Antonio Arruebo, Jonathan Gorremans and Raffaele Rossi (SolarPower Europe); Debbie Gray and Rebecca Ellis (International Hydropower Association); Jonas Moberg and Simran Sinha (Green Hydrogen Organisation); Mohamed Jameel Al Ramahi and Nikolas Meitanis (Masdar).

The report was developed with the support of the Boston Consulting Group. The authors wish to thank Rich Lesser, Michel Fredeau, Pattabi Seshadri, Tamer Obied, Vishal Mehta, Lars Holm, Ali Houjeij, Maria Agostini and Sasha Riser.

Communications and digitalisation support were provided by Nicole Bockstaller, Daria Gazzola and Manuela Stefanides (IRENA); the COP28 Communications team; and Alexander Bath (GRA). The report was produced by IRENA, with graphic design by weeks.de Werbeagentur GmbH.

RENEWABLE POWER

Our success in reducing greenhouse gas emissions this decade will determine whether global temperature rise can be limited to 1.5°C. According to IRENA’s World Energy Transitions Outlook 2023, global energy-related CO2 emissions would need to decline significantly to 23 gigatonnes of CO2 (GtCO2) in 2030, from the record high of 36.8 GtCO2 in 2022 (IRENA, 2023a).

IRENA’s 1.5°C Scenario identifies a technically and economically feasible pathway to an energy future that is consistent with Paris Agreement goals. It concludes that energy efficiency and electrification powered by renewables, clean hydrogen and direct use of renewables are driving the transition; but the sheer scale and extent of this transition requires a rapid and systemic transformation of the energy system.

Despite the progress achieved to date, the current deployment of energy transition technologies is insufficient in speed and scale to achieve the Paris Agreement goals. The energy transition requires an urgent and significant acceleration across energy supply, end-use sectors and enabling technologies – particularly the deployment of renewable power generation systems in more countries and regions.

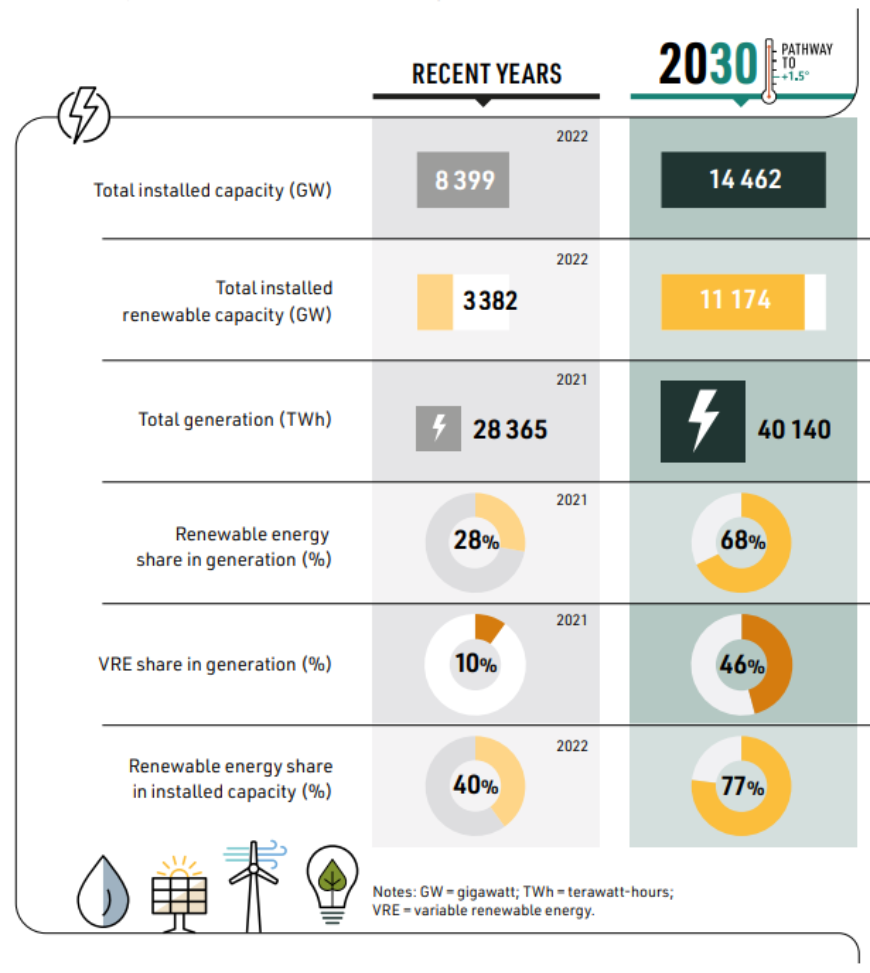

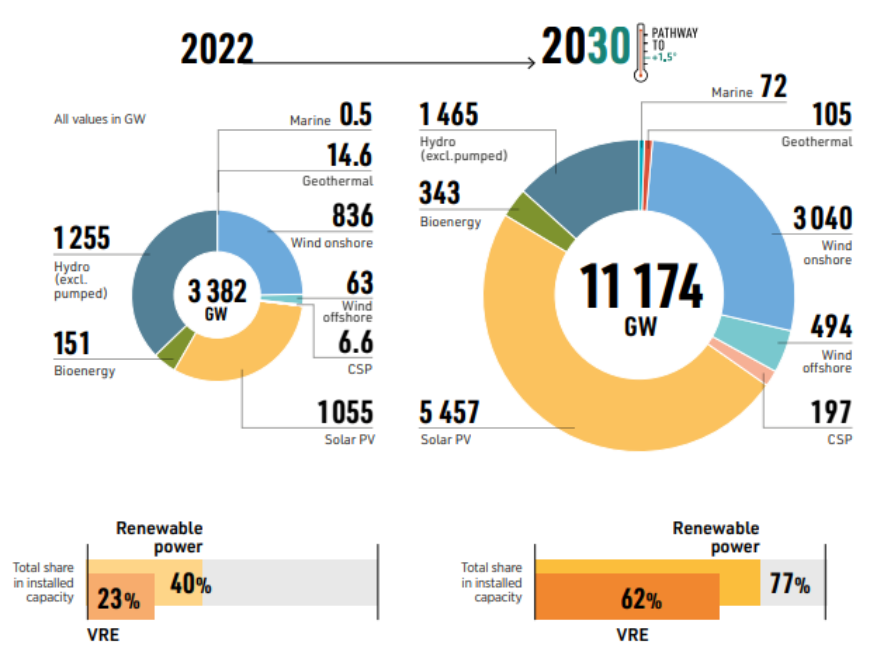

By 2030, global total installed renewable power generation capacity would need to expand more than three-fold, from 3 382 GW in 2022 to 11 174 GW, according to IRENA’s 1.5°C Scenario. Specifically, installed solar PV capacity would rise to more than 5 400 GW, from 1 055 GW in 2022, and wind installations would surpass 3 500 GW (3 040 GW onshore and 500 GW offshore), up from 899 GW in 2022, over the same period (IRENA, 2023a, 2023c). The share of variable renewable energy (VRE) – such as solar PV and wind power – in electricity generation would rise from 10% of the total electricity generated in 2021 to 46% by 2030, requiring additional flexibility in the operation of the energy system. After solar PV and wind power, the third-largest increase in generation capacity would be in hydropower; by 2030, global installed hydropower capacity (excluding pumped hydro) would grow by almost 17% from the 2022 level, reaching 1 465 GW under the IRENA 1.5°C Scenario.

FIGURE 1 Key performance indicators for achieving the 1.5°C Scenario in the Decade for Action

This suggests average renewable energy capacity additions of approximately 1 000 GW each year in the current decade – more than three times the installed renewable capacity added in 2022 (292 GW, including 189 GW of solar and 73 GW of wind power) (IRENA, 2023c). With average annual additions of 551 GW of solar PV and 329 GW of wind power to 2030, solar PV and wind power would dominate annual power generation capacity additions this decade. Energy storage capacity would expand in tandem, with cumulative global battery storage increasing by a factor of 21, from 17 GW in 2020 to 359 GW in 2030 (IRENA, 2023a).

Renewable power additions this decade may not be linear, however, with many factors impacting the rate of growth. Given that annual installation levels in 2022 were less than one-third of the 1 000 GW average annual installation rate required to 2030 under IRENA’s 1.5°C Scenario, growth of renewable power technologies over the remaining period of this decade will need to accelerate immediately (IRENA, 2023a). Some projections of solar growth foresee that 1 000 GW of annual solar PV installations alone may be reached as soon as 2028 (Haegel et al., 2023). To meet the tripling renewable power target, annual renewable additions need to ramp up as fast as possible, and as early as possible, in this decade.

Countries and regions will follow different trajectories in accelerating the deployment of renewable power capacity. Those with lower barriers to investment, higher renewable energy resource potential and more mature power markets – among other key enabling factors – should aim for greater increases in renewable capacity and economy decarbonisation. This will allow them to assist others by sharing lessons learnt, technological and technical know-how, and experiences in establishing the right conditions for the scaling up of renewables.

Under the IRENA 1.5°C Scenario, the global solar PV market would be dominated by G20 countries; but outside this group, cumulative capacity will need to surpass 900 GW by 2030, while the cumulative capacity in G20 countries would reach approximately 4 530 GW. For wind, China, the United States, Canada, Brazil and several European countries have high onshore wind potential, while the majority of expansions in offshore wind would be in four key markets (China, EU-27, the United States and India), accounting for more than 60% of offshore wind deployment by 2030. For hydropower, G20 countries together would account for 79% (over 1 150 GW) of global hydropower capacity by 2030, with almost 305 GW of total capacity spread across the rest of the world.

FIGURE 2 Global installed renewable electricity generation capacity in the 1.5°C Scenario, 2022 and 2030

Based on: (IRENA, 2023a).

It is important that renewable power generation capacity, including both grid-connected and off-grid systems, expands more rapidly in the developing world, given its growing electricity demand; renewables can – and should – play an important role in addressing the significant energy access deficit in developing countries, through both grid and off-grid applications. Currently, despite vast potential, many developing countries are lagging behind in terms of their deployment of renewable power systems and related investments; for instance, of the cumulative investment of USD 2 841 billion in renewable energy in 2000–2020 worldwide, Africa only received USD 60 billion, or 2% (IRENA and AfDB, 2022).

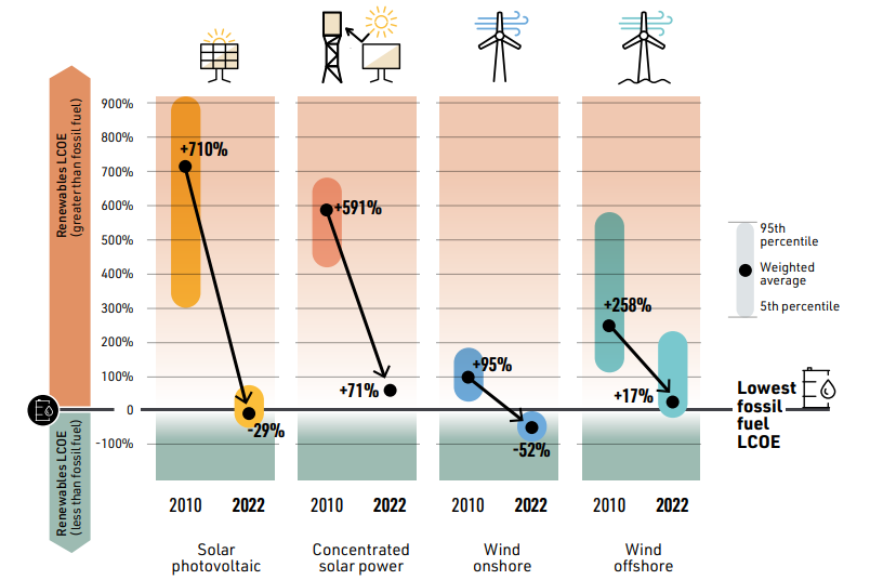

Accelerating renewable power deployment is not only beneficial from a climate perspective; the economic case for this acceleration is now compelling, given the dramatic improvements in the competitiveness of renewable energy sources such as solar and wind power.

In 2010, the global weighted average levelised cost of electricity (LCOE) of onshore wind was USD 0.107/kilowatt hour (kWh) – 95% higher than the lowest fossil fuel cost of USD 0.056/kWh. Yet, by 2022, the global weighted average LCOE of new onshore wind projects was USD 0.033/kWh – 52% lower than the cheapest fossil fuel-fired option, at USD 0.069/kWh (Figure 3).

This improvement was surpassed by that of solar PV, however. In 2010, solar PV had a global weighted average LCOE of USD 0.445/kWh – 710% more expensive than the cheapest fossil fuel-fired option; but by 2022, a spectacular decline in costs – to USD 0.049/kWh – made solar PV’s global weighted average LCOE 29% lower than the cheapest fossil fuel-fired option (IRENA, 2023b).

FIGURE 3 Cost competitiveness of solar and wind power, 2010-2022

Based on: (IRENA, 2023a).

The global weighted-average LCOE of offshore wind fell from being 258% more expensive than the cheapest fossil fuel option in 2010 to being just 17% more expensive in 2022, with costs falling from USD 0.197/kWh to USD 0.081/kWh. Concentrated solar power (CSP) saw its global weighted average LCOE fall from 591% higher than the cheapest fossil fuel option in 2010 to 71% higher in 2022 (IRENA, 2023b).

While hydropower’s global weighted average LCOE increased in 2021-2022 to USD 0.061/kWh – largely owing to the development of more challenging and remote sites – it remains cheaper than new fossil-fuel fired options. This is also true for geothermal projects, with a global weighted-average LCOE of USD 0.056/kWh in 2022, as well as for bioenergy projects, at USD 0.061/kWh (IRENA, 2023b).

It is equally important to consider the wider economic and environmental benefits of renewable power in reducing fossil fuel imports, improving a country’s balance of payments and enhancing security of affordable energy supply by reducing exposure to volatile fossil fuel prices in global markets. 2 As 2022 showed, the indirect economic benefits of this enhanced energy security can be significant; yet they are typically not valued in current policy.

FIGURE 4 Investments required to meet the 1.5°C goal

Similarly, the economic benefits of reducing pollution, and thereby improving climate, environmental and health outcomes, are almost never properly valued in policy-setting (IRENA, 2023b). These unpriced benefits significantly improve the competitiveness of renewable power and make the business case for accelerated deployment even more compelling.

Under IRENA’s 1.5°C Scenario, the power systems of tomorrow would integrate a broad range of renewable sources, with each technology playing a key role in meeting electricity demand; but solar and wind power will dominate capacity expansion. This represents a transformative shift in power system supply dynamics and poses new challenges to power system operations. These may be met by adopting new operational strategies and mechanisms, accelerating the scale-up of smart demand response schemes and deploying technologies that support power system flexibility, including hydropower with reservoirs and pumped storage; energy storage; and sector coupling technologies.

In recent years, hydrogen produced from renewable electricity – known as ‘green hydrogen’ – and its derivatives have been identified as industrial feedstocks for decarbonising hard-to-abate sectors. Hydrogen has also been recognised as an energy carrier that can be used to balance electricity demand with supply from variable renewable energy, thereby providing the increasing flexibility required by grids. Scaling up green hydrogen therefore offers significant potential for integrating higher shares of renewable energy in grids, and can also provide a solution for seasonal energy storage.

ENERGY EFFICIENCY

A rapid scale-up in renewables is only part of the energy transition equation. The transition should also aim to deliver reduced energy intensity across the economy through a range of more energy efficient technologies, complemented by structural and behavioural changes. These measures can often generate economic and environmental co-benefits. A range of measures will be needed across all end-use sectors, including modal shifts from private passenger cars to collective transport, and from passenger aviation and road-based freight to rail, as well as the adoption of circular economy principles, improved building insulation, heat pumps and efficient electric motors – especially for industrial end-use sectors.

Energy efficiency (measured in terms of energy intensity improvement rates 3 ) in IRENA’s 1.5°C Scenario is largely a result of a combination of efficient technologies in end-use sectors and extensive electrification. The electrification of end-use sectors – such as in transport and buildings – would see a rise in direct use of electricity in total final energy consumption from 22% in 2020 to 29% in 2030.

Technical energy efficiency improvements embodied by heat pumps, more efficient appliances and electric vehicles – together with flexible, smart electrification strategies and deployment of decentralised energy – are of tremendous importance in decarbonising end-use sectors such as buildings and transportation. For industrial sectors, continued energy efficiency improvements play an important role in keeping the overall energy consumption by industry close to unchanged in 2050 from present levels (IRENA, 2023a).

To align with IRENA’s 1.5°C Scenario, the global annual rate of energy intensity improvement should double by 2030 from the current level, which is also in line with the assessment of the International Energy Agency (IEA, 2023). If this rate is achieved, global final energy consumption would experience minimal growth over the same period.

With renewables and energy efficiency best placed to meet climate commitments as well as energy security and energy affordability objectives, governments must redouble their efforts to ensure sufficient investments are made.

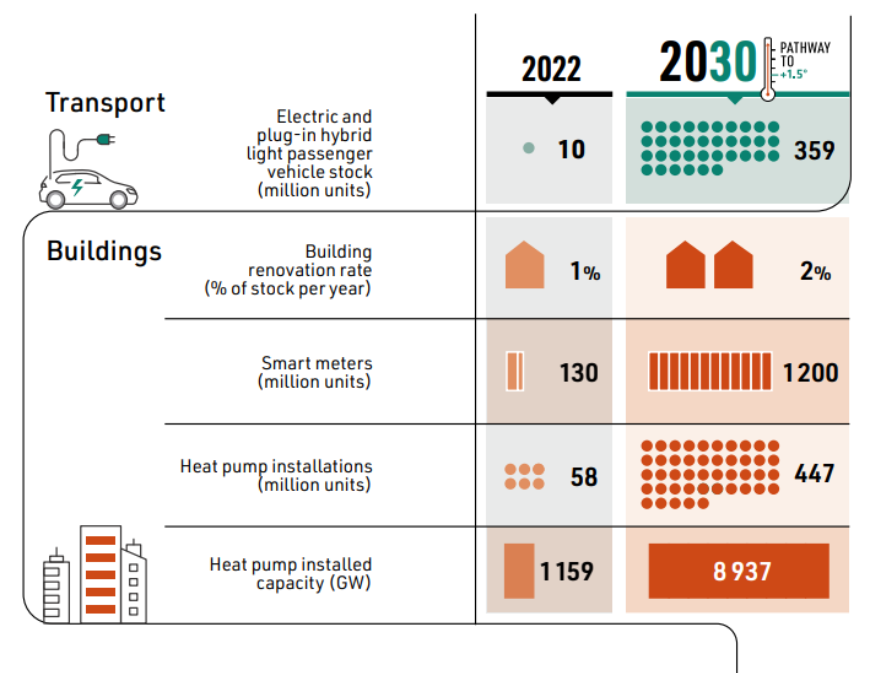

FIGURE 5 Energy intensity: Indicators in transport and buildings in 2030

INFRASTRUCTURE AND SYSTEM OPERATION

Wind and solar power are the fastest growing sources of power worldwide, but there is also a need to accommodate a more diverse range of renewable energy sources in the power mix – including hydropower with reservoir storage and biomass-based power plants. This will require enhancements to – and expansion of – current power grid systems, and the modernisation and upgrading of power system operations.

With VRE sources becoming the major source of power in a 1.5°C-compatible world, countries must start upgrading and expanding their power grid infrastructure to prepare for increasing end-use sector electrification. Multiple measures are required, including:

- Innovative power planning, grid expansion, modernisation and enhancement, and addressing interconnection backlogs (projects awaiting connection to the grid).

- Changes in grid operation and management, potentially also including new market design.

- Increased interconnectors between countries and regions.

- Growth in electricity storage; comprising short-duration storage for increasing grid flexibility and long-duration storage to enhance energy security (e.g. pumped storage).

- Measures to allow greater integration of demand-side management and behind-the-meter (consumer) flexibility options (e.g. distributed storage).

- Introducing other flexibility sources (e.g. green hydrogen, hybrid renewable parks combining wind/solar/storage, etc.).

FIGURE 6

Power grids

Investments in the electricity grid have lagged behind those in renewable power and must now significantly ramp up in anticipation of the considerable renewable power additions required. Countries need to prepare for the large amounts of VRE that will come online in the next few decades, as grid investments must be made 3-5 years before renewable energy investments to mitigate the overall system costs of greater renewable penetration (LBNL, 2022). 4 With clarity on grid infrastructure development plans and reasonable guarantees on connection availability, investors will feel more confident building new generation; meanwhile, consumers would be more likely to invest in electrification when a reliable supply of low-cost electricity can be made available.

When integrating higher shares of locally available variable solar and wind power, power systems will also need to innovate to become: increasingly decentralised, allowing electricity to be generated at locations closer to demand; and bi-directional, allowing electricity from distributed power generating facilities to be injected into the grid.

Modernised, smarter grids are required; in the European Union (EU), around 30% of the envisaged investment in grids by 2030 could be earmarked for digitalisation 5 (European Commission, 2022). They will also need to be larger and more robust. Hence, grid costs are expected to increase over time (IRENA, 2023a). This will require fast-tracked permitting to ensure timely investments in modern grids. Adding more widely distributed power generation sources will also bring resilience, especially against increasingly intense extreme weather events owing to climate change (IPCC, 2023).

The electrification of transport also requires significant investments in enabling infrastructure. Electric vehicles will potentially account for more than 80% of all road transport activity by 2050; with 359 million electric and plug-in hybrid light passenger vehicles worldwide by 2030 and 2 182 million by 2050 (IRENA, 2023a); yet their market entry will be contingent upon coordinated investments in charging infrastructure and power grids.

URGENT RECOMMENDATIONS FOR POLICY MAKERS

- Ensure planning, timelines and assessments of investment needs for grids are aligned with long-term targets for renewable energy buildout and end-use sector decarbonisation, e.g. transport.

- Mobilise funds for long-term grid investment; channel donor finance to building capacity and infrastructure for integrating renewables; and streamline permitting procedures for new grid infrastructure and upgrades to existing transmission and distribution infrastructure.

- Develop modernised, decentralised (where suitable) and more resilient grid systems using digitalisation, smart applications for demand-side management and interconnections with neighbouring grid systems.

Energy storage

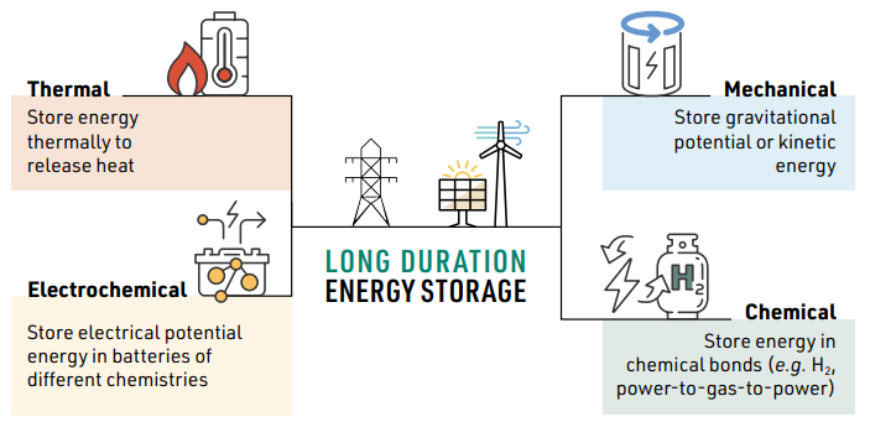

With a growing share of variable renewable power generation, energy storage is needed to ensure the electricity generated is successfully delivered when shortfalls between supply and demand occur. Historically, this has been provided by pumped storage and hydropower with reservoirs. However, there are now many types of storage, including electro-chemical storage (batteries), thermal energy storage (which employs rocks, bricks or molten salts to store heat), mechanical technologies (employing compressed air, liquid air or gravitational potential) and chemical storage (storing energy in chemical bonds such as hydrogen or its derivatives). All of these technologies are undergoing rapid innovation.

FIGURE 7: Long duration energy storage technologies

Long-duration energy storage (LDES) provides the means to store energy for hours, 6 days, weeks or even seasons when renewable generation is abundant relative to load, and releasing it when demand is greater than generation (e.g. saving energy from spring days with low loads and abundant solar to deploy during high load days in the summer; or from windy autumn days to deploy during high load cloudy winter days). Diverse storage technologies enhance the resilience of grids that are subject to extreme weather for prolonged periods, help relieve grid congestion, provide transmission services and shore up local area reliability.

LDES, including storage technologies spanning 10+, 24+, 100+ and 150+ hours in duration and providing both power and heat, is also able to provide other grid services including black start (restarting parts of the grid where power has been lost in a blackout) and micro-grid level assistance for areas or key infrastructure that may lose power. Storage durations can span weeks or months in the case of pumped storage and reservoir hydropower. As the largest form of installed flexibility at over 175 GW worldwide, pumped storage hydropower can play an important role in providing LDES and vital grid services, with substantial potential for off-river pumped storage to be developed in the coming decades (IHA, 2023). Some LDES technologies are commercially available today, while others are still in the early stages of development. Numerous companies are signing contracts (e.g. with utilities, airports, data centres, industrial users, etc.) and are deploying LDES at grid-scale quantities, and pumped storage has been successfully deployed for decades.

One emerging LDES technology is hydrogen storage. Hydrogen’s true competitive strength lies in its unique ability to store energy for long periods of time in large quantities. As green hydrogen displaces fossil fuels in some end uses, hydrogen storage could become increasingly critical to energy security, in the same way that natural gas storage is today in many regions. Hydrogen storage will be needed primarily to meet variation in supply (rather than demand), as green hydrogen is created using VRE sources. Long-term hydrogen storage can play an important role in strengthening energy security and system resilience (IRENA, 2023d). Support for the continued development of these technologies is critical for decarbonisation.

In many places, however, legacy market arrangements and policy frameworks do not incentivise investment in storage at scale. Action from policy makers can drive progress in this sector, such as: assessing energy storage and flexibility needs; setting LDES mandates for medium- and long-term capacity targets; updating criteria for marketplaces; providing innovation grants and subsidies for prefeasibility studies; and establishing public-private partnerships.

Other market innovations can also foster a healthy storage market, such as the introduction of congestion management trading platforms, ancillary services markets to support the grid, and awarding additional value for features such as flexibility in capacity payments and capability to provide peaking power (e.g. storage technologies that can replace a natural gas peaking plant should be reflected in system modelling).

URGENT RECOMMENDATIONS FOR POLICY MAKERS

- Conduct technical assessments of system decarbonisation needs and timelines, and ensure the planned buildout of renewables is complemented by storage resources of varying duration, as well as other sources of flexibility.

- Collaborate with regulators and the renewables sector to enhance power market planning and ensure price signals, clear targets and procurement incentivise longer duration storage.

- Encourage investment and innovation in diverse storage technologies to suit different users, such as by establishing research, development and innovation (RDI) grant programmes, encouraging public–private partnerships and setting medium- and long-term capacity targets.

End-use electrification and sector coupling

With solar and wind power scaling up rapidly in this decade, electrification has become a vital decarbonisation pathway. Green hydrogen and its derivatives, produced by electrolysers using low-cost renewable power, can be used to decarbonise end-use sectors that are difficult to electrify directly – such as iron and steel making, and shipping – and to provide seasonal energy storage solutions.

However, electrification needs to be accelerated by systemic innovation, making it not only faster but smarter. Smart electrification – through sector coupling and enhanced flexibility – prevents a higher peak electricity load on the power system. It also enables the power system to accommodate new loads while allowing integration of a higher share of variable renewable electricity in a cost-efficient manner. This can help sustain renewables-based electrification without jeopardising energy system operation, thus making the power system robust and resilient. To harness all these benefits, systemic innovation should involve the entire energy value chain across four key dimensions: technology and infrastructure; market design and regulation; system planning and operation; and business models (IRENA, 2023d). Smart charging for electric vehicles is a good example in this regard.

Sector coupling (integrating electricity grids, transport systems, heating in buildings and thermal energy grids) provides more opportunities to economically optimise overall operation as a single system, provided that the economic incentives are put in place and upgraded energy management systems are available (IRENA Coalition for Action, 2022).

The benefit of this will be smarter, more intelligent demand-side management, achieved by deploying more advanced digital technologies both behind-the-meter (by energy consumers) and in power systems. Demand response would become more agile and inter-operational through sector-coupled technologies such as energy storage systems and electric vehicles (EVs) connected to smart charging facilities. This would enable increased integration of variable renewable electricity in local energy networks and maximise overall benefits by automating the monitoring and operation of assets (IRENA, 2021a; IRENA Coalition for Action, 2022).

End-use electrification, sector-coupling and the rapid scale-up of variable renewable electricity all require integrated cross-sectoral infrastructure planning – a process for optimising the co-development of increasingly connected infrastructure in various sectors. 7 The European Hotmaps project offers an open-source toolbox to support public authorities, energy agencies and urban planners as they plan heating and cooling at local, regional and national levels. It allows users to map cooling and heating demand, as well as supply, in the 27 EU Member States and the United Kingdom, and provides renewable energy generation and industrial waste heat potentials (Hotmaps, 2021). This facilitates the integration of heating and cooling with waste-to-energy and renewable energy, including power-to-heat. However, this planning approach requires incentives for infrastructure investments where market barriers exist, given that different infrastructures operate under different legislative, regulatory and policy regimes.

URGENT RECOMMENDATIONS FOR POLICY MAKERS

- Adopt a sector-coupling approach to the decarbonisation of economies by pursuing smart electrification of the transport, buildings and industry sectors.

- Create fora for co-ordinated planning among relevant authorities on infrastructure development, including renewable energy projects, grid and transmission assets, electric vehicle charging infrastructure and heat networks.

- Introduce economic incentives for smart electrification and demand-side response (such as tax credits and innovation grants) to encourage private investment in sector-coupling solutions.

Demand-side management

Electricity systems are complex; in addition to the grid infrastructure planning required to unlock the benefits of sector coupling, distributed grid planning and operations will need well-defined energy management schemes on both sides of the end-user meter. These schemes apply to both the supply side (power management) and demand side (load management).

Demand-side management (DSM) comprises a set of strategies traditionally aimed at reducing peak demand, which will be increasingly needed to incentivise consumption in periods of high VRE generation. DSM addresses various challenges, including VRE integration, rising electricity costs and environmental impacts. For example, DSM can employ time-of-use pricing to encourage customers to shift electricity usage to off-peak hours, while demand response programmes can financially reward customers for reducing electricity usage during peak hours or consuming electricity during high VRE generation periods. Critical-peak pricing, real-time pricing and critical-peak rebates are also among the strategies available. These approaches are crucial for optimising energy efficiency in both residential and industrial buildings.

As the transition advances, DSM will also provide flexibility to alleviate the need for more costly requirements. Several challenges persist, however – particularly in Latin America, the Middle East and North Africa, and other Global South regions. Notable issues include physical grid and digital technology infrastructure gaps, as well as complex and inconsistent regulations and policies. Financing challenges also hinder progress; attracting investment in clean energy enablers like DSM solutions requires innovative financing models and incentives.

Intelligent load control, demand response and energy efficiency are pivotal in enabling a secure and resilient renewables-based power system. Continued investment and innovation in these areas will further drive the adaptation of demand to supply in a renewable energy-driven future.

URGENT RECOMMENDATIONS FOR POLICY MAKERS

- Assess the cost-benefit of investment in DSM programmes, accounting for the energy and cost savings it can provide instead of investing in grid infrastructure expansion.

- Ensure grid planning prioritises modernisation and DSM technology to close critical technology gaps as infrastructure expands. Developing economies can explore innovative financing models – such as blended finance – to mobilise investment in grid and DSM solutions.

- Improve data availability within the wider electricity system to enable innovation in DSM and access to applications like smart meters by consumers and third parties.

POLICY AND REGULATION

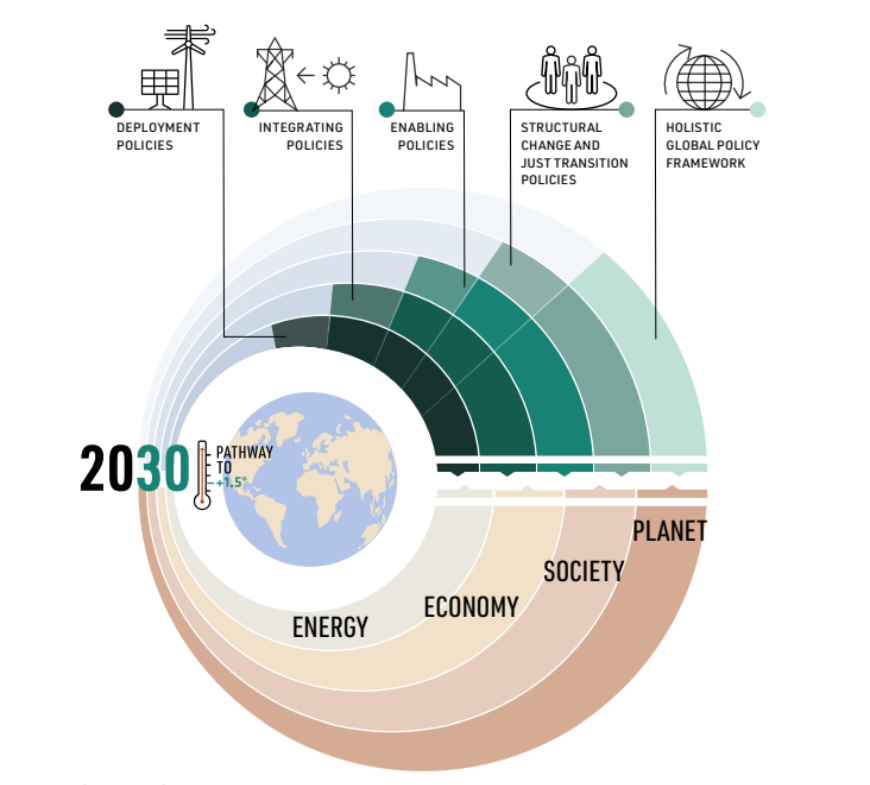

Governments have a crucial role to play in tripling renewable power capacity and placing the world on a 1.5°C pathway. All too often, the energy transition discourse relegates governments’ responsibilities to creating an enabling environment for private investments through predictable and stable policies, and the creation of instruments that de-risk investment projects. Although this is crucial, a much broader and more integrated policy approach is required to facilitate the adoption of an entire spectrum of energy transition solutions needed to achieve the 1.5°C target and unlock its socio-economic benefits (Figure 8).

Governments need to be far more engaged in shaping and guiding the energy transition, including through policies for ambitious public investment programmes and sufficient forward-planning for renewables scale-up, system integration and grid build-out.

Cross-cutting approaches covering all renewable technologies, electrification technologies and others are needed to facilitate the energy transition (e.g. energy storage), include enabling policies that set ambitions and send clear signals to stakeholders, eliminate distortions, incentivise the uptake of solutions and facilitate access to affordable financing. They also include policies that ensure the integration of renewables within energy systems, economies, nature and societies, as well as specific deployment policies for various technologies. Planning for transmission infrastructure, inter-regional power trading, workforce recruitment and training, flexibility services and end-use sector decarbonisation should all be aligned with overall climate and renewable energy targets to ensure renewable power can be efficiently integrated and dispatched to areas of demand.

Transitioning to a renewables-based economy may also bring challenges in the form of financing gaps, labour market disruptions and energy sector insecurity. These misalignments, if not well-managed, risk inequitable outcomes and a slower pace of the energy transition. Therefore, a set of structural and just transition policies, along with the creation of strong institutions to ensure policy co-ordination and cohesion, is required to manage potential misalignments.

Finally, a holistic global policy framework that entails international collaboration including North-South and South-South co-operation is needed to bring stakeholders from countries around the world together to commit to a just transition that leaves no one behind and strengthens international finance flows, capacities and technologies in an equitable manner.

This section focuses on the key policies and regulations needed to accelerate energy efficiency and renewable power technologies; phase down fossil fuel generation and replace inefficient equipment; shape power market design to integrate higher shares of renewables; and maximise social and environmental benefits.

FIGURE 8 The IRENA holistic policy framework for a just and inclusive energy transition

Improving energy efficiency

Improving energy efficiency could deliver around a quarter of the emissions reductions needed by 2050, according to IRENA’s 1.5°C Scenario. Enhanced energy efficiency is a crucial enabler for making high levels of end-use electrification feasible and affordable. Measures related to reducing energy demand and improving efficiency are needed across all end-use sectors.

Minimum energy performance standards (MEPS) can support industrial, commercial and residential users to procure and switch to more energy efficient appliances or equipment such as electric heating/ cooling technologies. Building codes can set energy performance requirements by specifying insulation standards, thereby reducing heating and cooling demands. They can also specify greenhouse gas emission targets and carbon footprints. For renovation, in particular, codes can be coupled with financial incentives.

It is also important to address prevailing challenges associated with building ownership structures, equitable access and benefit-sharing of energy efficiency investments and policies. “Green loans” could carry lower interest rates and protect low-income energy consumers from energy price fluctuations and inflationary environments. Awareness campaigns for end-users also play an important role in the adoption of energy efficiency and energy conservation measures.

In the transport sector, significant improvements can be achieved by promoting energy efficient mobility (e.g. public transport such as railways, metros and buses, and car-sharing), as well as active (nonmotorised) transport such as cycling and walking in urban areas. Public campaigns can be undertaken by national and local governments to encourage green mobility modes. Other policies, such as differentiated parking fees and highway tolls, can encourage a shift to public transport, complemented by dedicated driving lanes for car-sharing. Public transportation fleets also offer the opportunity to utilise costcompetitive renewable fuels or electricity.

URGENT RECOMMENDATIONS FOR POLICY MAKERS

- Adopt ambitious targets for energy efficiency improvement with specific time horizons and outline clear avenues for implementation.

- Strengthen regulatory frameworks, including building codes that specify low energy performance and appliance energy efficiency standards.

- Expand the availability of financial incentives and affordable lending schemes for meeting standards on energy efficiency, such as tax credits or green loans with favourable interest rates for building renovation or modernisation.

- Establish public campaigns to build awareness of the role of energy efficiency measures, public transport and green mobility for cost savings and collective decarbonisation goals.

Market incentives and fiscal policy

While renewables have become increasingly competitive, they still face barriers compared to fossil fuels. Rising fossil fuel prices have acted as an important catalyst for energy efficiency measures; yet, energy efficiency improvements and renewables deployment still face financial and other obstacles, such as access to capital or long pay-back periods. Fiscal and regulatory incentives therefore play an important role in accelerating the deployment of both renewable energy and energy efficiency measures.

A progressive, supportive fiscal system can be achieved by eliminating market structures that favour the uptake of fossil fuels (e.g. phasing out direct and indirect fossil fuel subsidies) and reflecting environmental and social costs associated with the use of fossil fuels through taxation or other mechanisms. Such policies would improve the economic competitiveness of renewable energy and energy efficiency solutions.

Taxes and levies, subsidies or exemptions on duties for imported/exported components required by the renewables sector could kickstart private investment in renewables projects and manufacturing activity. Countries with fiscal restraints can benefit from donor finance to support building capacity and physical infrastructure for the integration of renewable power, among other important aspects that would assist those countries in advancing the energy transition.

The energy transition will only succeed if it is both deep and broad. Therefore, careful consideration of broader social and equity issues is also vital, particularly for low-income populations for whom energy constitutes a larger share of household expenditure. Financial support drawn from general taxation, tax on windfall profits and ongoing taxation of fossil fuel energy production and carbon pricing revenue can all be used to support the transition.

Regulatory policies, such as tariff-based procurement mechanisms – e.g. feed-in tariffs or auction schemes using a contracts for difference (CfD) mechanism, which provide stable prices over long periods – are also effective. The choice of instrument and its design should consider: the nature of the solution (e.g. utility-scale, distributed, off-grid); level of development of the sector; power system organisational structure; wider macroeconomic environment (e.g. impact of inflation and commodity price volatility); and broader policy objectives. It is important that price levels for public procurement schemes – and competitive auctions in particular – balance cost-efficient electricity supply to consumers with healthy, sustainable supply chain development for the renewables sector. However, any trade-offs in these areas must carefully consider the risk of non-delivery, given the very tight timeline to achieve the renewable power and energy efficiency targets for 2030.

Private investments will continue to play a major role in the energy transition. As such, it is vital that policy makers ensure a policy and regulatory environment that de-risks investments and unlocks private capital flows to the renewables sector. Key factors include setting clear and ambitious capacity targets with a rolling schedule for procurement, as well as ensuring large volumes of land/seabed are made available – where under government control – for renewables development, and that permitting and environmental processes are efficient and streamlined (see below). This will help to provide predictability for investors, developers and supply chain actors, while enabling public authorities to efficiently plan for grid integration, workforce development and demand-side management.

Where procurement is facilitated by CfDs, power purchase agreements (PPAs) or other mechanisms, these should meet international standards for bankability in terms of their coverage of dispute mechanisms, grid connection delays and curtailment risk. A mechanism to allow for bilateral power procurement between generators and private off-takers (such as industrial actors or corporates) can further strengthen the case for large deployment volumes.

URGENT RECOMMENDATIONS FOR POLICY MAKERS

- Ensure fiscal policy prioritises equity in the energy transition, for instance by investing proceeds from taxes on fossil fuel energy production and carbon pricing mechanisms in enabling infrastructure, or supplementing clean electricity access for low-income populations via green financing schemes and other instruments.

- Introduce tax credits, levies and/or exemptions on import/export duties for key materials and components in the renewable energy supply chain.

- Ensure procurement schemes, including tenders, provide adequate price signals for investment and balance long-term price/cost risk mitigation with socio-economic value creation, thereby providing cost-efficient electricity, and enabling forward-planning and investment in renewable energy supply chains.

- Consider the trade-offs between ‘lowest-price’ objectives, and other policy outcomes such as socio-economic development, system integration and industry sustainability.

Power market design and regulation

The world is entering a new era in which electricity systems will be increasingly dominated by zeromarginal-cost renewable technologies. Power markets must evolve and adapt to new market forces, such as corporate and industrial demand, and behind-the-meter (prosumer) generation. They must be organised in a way that incentivises new investment in renewable power generation and the flexibility to provide reliable electricity at a level required for the 1.5°C pathway. This requires governments and other stakeholders to undertake a close examination of their power systems’ organisational structures, i.e. the institutions, processes and arrangements through which electricity services are exchanged and rewarded.

Wholesale power markets today are based on marginal cost pricing, where the most expensive generator (with the highest variable cost – typically fossil fuel-fired plants) determines electricity prices for the time period in which the market operates. This poses a number of challenges. As the share of renewable power grows, wholesale spot markets will see increased price volatility, as periods of high renewable power generation push clearing prices in the wholesale market close to zero. When renewable generation is less than demand, flexibility resources will be needed, potentially resulting in very high prices at certain times.

If wholesale markets are the main source of revenue, the economic feasibility of new investments will plummet, as even existing generators will struggle to recover their initial capital costs whilst prospective investors realise diminishing returns. The paradigm that relies on free markets to incentivise power supply investment decisions therefore needs to change.

Ultimately, a renewables-based power system requires enhanced flexibility; wholesale market design must deliver this as well as providing the volume of renewable power needed. Policy makers must therefore urgently create the enabling conditions for power grid and system flexibility to integrate increasing shares of wind, solar and other forms of renewable energy.

Power system organisational structures must evolve to better align with energy policy and decarbonisation goals. A “dual procurement” power market design could introduce long-term contract mechanisms (e.g. Auctions, CfDs, PPAs) as the backbone of renewable power procurement, alongside a short-term market to dispatch flexible resources in an affordable way (IRENA, 2022a). This holistic model would incentivise continued investment in large-scale, capital-intensive renewable energy projects, while assuring the flexibility needed for a resilient and reliable renewables-based power system.

This transformation is partially underway, as auctions are becoming the preferred tool to procure renewable energy, and wholesale markets are becoming more time and location granular (IRENA, 2023a); but there are meaningful actions authorities can take now to ensure the acceleration of this trend.

One way to achieve enhanced system flexibility is for power markets to allow flexibility technologies (such as batteries and pumped hydropower) to provide ancillary services and be rewarded accordingly. Ancillary services that serve to stabilise the grid network and will become increasingly important as dispatchable fossil fuel-based generation is phased out of the power mix. Today, many power systems reward the provision of energy but not ancillary services (where these services are not included in contractual obligations). They therefore need to be appropriately valued and reflected in power system design. Valuing, pricing and procuring ancillary services astutely can bring new players to the grid, with advantages for the whole power system. Examples of this include the enhanced frequency regulation auctions in the UK.

To achieve the energy transition, individuals, communities and businesses will also need to become active participants in the energy system. This includes growth in distributed renewable energy generation systems – notably using solar PV – but also community solar and wind projects. This will require electrical grids that allow energy consumers to easily install and utilise small- to mid-scale renewable energy projects to cover their consumption, and/or inject power into the grid through connection schemes like net-metering and feed-in-tariffs. Such measures can maximise the socio-economic benefits of renewable energy, insulate consumers from price volatility, create local supply chains and job opportunities, and enhance public perceptions of renewables.

URGENT RECOMMENDATIONS FOR POLICY MAKERS

- Ensure price signals encourage sufficient investment in additional renewable capacity to meet climate and energy transition targets; and adopt renewable power procurement approaches that recognise the net benefits and costs of social, environmental, system integration and energy security factors.

- Design auctions that balance competitive price discovery and long-term delivery of affordable electricity. Auctions should also be run for sufficiently large and ambitious volumes, with consistent, transparent tendering schedules to effectively foster competitive bidding.

- Create a capacity market for flexibility services (including ancillary services and storage capacities of varying duration) with a long time horizon aligned to targeted renewable energy penetration of the power mix.

- Rethink participation rules to allow new technologies to engage in the power market as flexibility providers, including storage and demand side aggregators.

- Encourage investment in distributed renewable energy systems that allow consumers to become “prosumers” by both using and producing clean electricity.

- Reorganise power market structures to ensure policies for accelerating renewables deployment account for system flexibility as well as sustainable returns to generators and investors.

Streamlining permitting

The time and cost constraints imposed by permitting procedures represent a major bottleneck impacting the deployment of renewable energy projects in many countries. It is essential that permitting procedures are fit-for-purpose and keep pace with renewable and climate targets, without compromising environmental and social impact standards. Experiences from the public and private sectors indicate that best practices in permitting centre on four areas: administrative consolidation; digitalisation; policy support; and public engagement (European Commission, 2023).

Renewable energy developers often need to consult numerous authorities at national, sub-national and sometimes village or prefecture level for the necessary permits to build a project. This process can be lengthy and extremely bureaucratic; for instance, the global average time required for permitting an offshore wind project is nine years. Onshore wind and utility-scale PV permitting processes can also be long, although they are typically shorter than those for offshore wind. Similar obstacles exist for hydropower projects and smaller scale distributed projects for end consumers using renewable energy technologies like rooftop solar.

Creating dedicated, centralised authorities is one way to streamline this process by ensuring developers can refer to a single focal point. Countries like Denmark and the Philippines have already adopted a “one-stop shop” model to accelerate renewables deployment, but this model only works if it is adequately resourced. In addition, digitalised processes to submit and track applications would enable developments to progress more efficiently, while access to digitised local consenting and historical dispute records would allow developers and authorities to screen sites that could be high-risk or unsuitable at an early stage (IRENA, 2023h).

An overarching best practice is the introduction of legislation mandating a maximum lead time for the permitting of renewable energy projects. Revisions to the EU Renewable Energy Directive in 2023, for instance, set a maximum two-year lead time for permitting new renewables projects, and one year for repowering (refurbishing or replacing) wind and solar projects. Gaining social acceptance through public engagement with relevant stakeholders is critical in the consenting and constructing stages of a renewable energy project. This includes early and continuous consultation by authorities and developers with local communities to communicate the benefits and considerations brought by a project to the area, as well as a transparent conflict resolution mechanism that sincerely addresses community concerns.

Comprehensive and efficient permitting frameworks represent a clear win-win, allowing renewable energy development to expand this decade while cultivating acceptance with other interests in land and sea spaces. The Planning for Climate Commission has produced a nine-point plan for tackling climate change through fast and fair permitting for renewable energy and green hydrogen that provides best practices and can be consulted by policy makers worldwide (GHO, 2023).

Recent studies indicate that adopting best practices in permitting could cut consenting time for utility-scale wind and solar projects by more than half; for example, onshore wind farms could be permitted in one year, offshore wind farms in 1.5 years and solar farms in as little as three months (ETC, 2023). This makes permitting a high-impact enabler for the energy transition, where the necessary investment in resource, policy support and capacity will bring enormous value to countries in accelerating renewables growth and securing associated socio-economic and environmental benefits.

URGENT RECOMMENDATIONS FOR POLICY MAKERS

- Create a centralised authority to oversee permitting of renewables projects, consolidating information and requirements from all relevant authorities and issuing permits according to a transparent timeline.

- Mandate and enforce maximum lead times for applicants and authorities to complete the permitting stages of renewable energy projects, with discretionary additional time under exceptional circumstances for more complex projects.

- Allocate greater resources to permitting authorities, including human resources and investment in digitalisation and open-source databases, such as for land titles, mapping data and historical dispute records.

- Consider adopting efficient legal challenge processes by implementing a limited time window for raising disputes and establishing an authority to screen challenges, balancing public interests.

- Expedite processes for developers repowering assets on existing sites and provide the flexibility to adjust a proposed infrastructural, technological or social approach to projects without having to reapply for new permits.

Reducing negative impacts; maximising social and environmental benefits

Scaling up renewable energy deployment provides an opportunity to create widespread socio-economic benefits for communities around the world, including energy access, job creation, public health improvements and welfare generation. Renewable energy employment worldwide grew to an estimated 13.7 million direct and indirect jobs in 2022 (IRENA and ILO, 2023); under the 1.5°C pathway, tens of millions of additional jobs could be generated worldwide by 2030 (IRENA Coalition for Action, 2023).

The energy transition will bring benefits to any economy, but also challenges in the form of misalignments that may occur in finance, the labour force and the energy sector itself. If not well managed, these misalignments risk inequitable outcomes, which could sow doubt among policy makers and the public concerning the advantages of the transition and lead to a fractured and unco-ordinated policy environment. Hence, there is a need for policies and measures that equitably distribute the benefits of the energy transition and raise public awareness about these positive impacts.

In terms of jobs, sectoral misalignments may arise due to potential shifts in value and supply chains during the energy transition. For instance, transitioning from fossil fuel power generation to solar energy may shift the focus from fuel extraction to the semi-conductor industry. The impact on employment depends on factors such as domestic production and labour productivity. Labour-market interventions encompass adequate employment services attuned to evolving circumstances and needs, along with measures to facilitate labour mobility (IRENA and ILO, 2023).

Community benefit schemes span countries from Costa Rica to Mali and adopt a range of structures, from shared ownership of renewable assets to industry sponsorship of critical social and economic infrastructure in host communities (IRENA Coalition for Action, 2020). Under the right conditions and policies, citizen and community participation in renewable energy projects can accelerate deployment while boosting support for local energy transitions.

Aligning policies and measures with the principles of a just and equitable transition will facilitate local value creation and socio-economic benefits in host communities, and on a larger scale, ensure political and social stability as renewable energy expands.

As part of a sensitive and efficient permitting framework, renewable development must be well integrated with the principles of sustainability, circular economy and reduced environmental impact – particularly on land use and biodiversity. This also applies to enabling infrastructure, with grid expansion into remote and biodiverse areas requiring careful siting.

Adopting sustainable end-of-life management policies, including waste management legislation, can help countries prepare for the anticipated volumes of equipment waste such as solar PV panels and batteries. Research and development programmes across the energy and waste sectors, and industrial clusters, can help to further scale waste management infrastructure on a national or regional basis (IRENA and IEA, 2016).

URGENT RECOMMENDATIONS FOR POLICY MAKERS

- Align policies and measures with the principles of a just and equitable transition and foster local value creation and socio-economic benefits in host communities, with a special focus on the inclusion of marginalised groups.

- Anticipate labour market disruptions and establish programmes that can address workforce gaps, minimise labour misalignments, create opportunities for targeted recruitment and labour mobility, such as relocation grants, and establish social protection programmes.

- Minimise adverse environmental impacts and encourage nature-positive approaches, for example by incentivising the uptake of sustainability standards for new renewable energy assets – such as the Hydropower Sustainability Standard – as part of procurement schemes.

- Ensure the impacts of mining activities and the use of relatively scarce components are mitigated through provisions for circular economy (end-of-life management, recycling and reuse of materials).

- Gather information on renewables’ waste production through regular monitoring of waste produced by technology, the composition of waste streams, installed system performance and the causes and frequency of system failures, in order to adopt waste minimisation legislation suitable for the pace and scale of the transition.

SUPPLY CHAINS, SKILLS AND CAPACITIES

Building resilient supply chains

The vulnerabilities of key energy industries to logistics bottlenecks, commodity price volatility, trade barriers, and commodity and component import dependencies have become increasingly apparent in recent years. Energy supply chains have become a priority agenda for policy makers, as demand and competition for critical raw materials, rare earth elements and production capacity become more acute.

Without well-functioning and cost-efficient industrial supply chains, the energy transition will not materialise. If not well managed, competition, security and scarcity challenges in renewable energy supply chains could lead to a disorderly transition, characterised by slower rates of renewables deployment at inflated costs. A mismatch between supply and demand for several critical minerals is already evident, with particularly high levels observed for lithium – a key material required for the shortduration energy storage and electric transport sectors (IRENA, 2023e). Bottlenecks for key components in the wind industry – e.g. nacelles, blades and gearboxes – are set to emerge by the second half of this decade in Asia and the Americas (GWEC, 2023). High concentration risk in the global renewables supply chain also raises the prospect of price or security of supply uncertainty in the future.

Robust and resilient global supply chains are required to support a 1.5°C pathway. The mining and processing of critical materials including lithium, copper, nickel and other rare earth metals are constrained within specific geographies, exposing these supply chains to geopolitical tensions and concentration risks (IRENA, 2023e). Policy makers should work with the private sector to identify production gaps and supply chain weaknesses on a national and regional basis, and generate strategies to reinforce supply chain security.

Socially responsible procurement is another key issue, where many critical materials and components refined or manufactured in one country are imported by others for use in the renewables sector. It will be vital to ensure supply chains – in the mining and processing segments in particular – are managed with respect to fair trade, and high environmental, social governance (ESG) and sustainability standards. Resilient supply chains are also key to sustaining the cost-value proposition of renewable energy around the world.

As countries usher in large industrial policy packages for the energy transition, there is a risk of increasing barriers in the global exchange of renewable energy knowledge, innovation and technology transfer – all of which will be essential for a cost-effective and fair transition, particularly for emerging markets and developing economies. The need for local value creation and regional supply chain investment must be carefully balanced with reducing trade barriers for goods and services central to the renewables renewables industry. This will be key to avoid intensifying supply chain bottlenecks and making renewables less cost-competitive, while maximising socio-economic benefits.

Multilateral alignment of supply chain, trade and industrial policies for the energy transition will be important in creating unified standards and investment protocols that can channel capital to the renewables sector and nascent green hydrogen sector, and encourage best-in-class development standards. This will require governments to work with industry, civil society and other stakeholders to ensure supply chain planning is conducted through a wider lens that encompasses national interests, cost-effective and socially responsible sourcing, long-term social and environmental sustainability, and climate and renewable energy targets.

URGENT RECOMMENDATIONS FOR POLICY MAKERS

- Collaborate with the renewables industry on industrial development reviews and plans for the transition that are sustainable, achievable, and adequately mitigate risk of supply insecurity and price volatility. Approaches include diversifying sources of production, anticipating critical production gaps and localising value chains.

- Ensure socially responsible procurement of renewables by encouraging uptake of sustainable supply chain assurance schemes, such as the Solar Stewardship Initiative.

- Incentivise public–private partnerships and investment in circularity to encourage reuse of materials and a circular economy approach to project development, which can help to reduce concentration risk and supply insecurity of critical materials.

- Co-operate with international fora and financial institutions to safeguard international trade corridors for materials and components for key renewable energy technologies.

Education, training and capacity-building

Building a skilled energy transition workforce requires measures to both expand the talent pipeline and enhance the quality of education and training provisions.

Early exposure to renewable energy topics and careers is vital for sparking interest in pursuing a career in the sector, but also to increase social acceptance by a knowledgeable citizenry. The curricula at higher education and vocational training institutions must reflect the skills and competences required by the transition.

In addition to strengthening the content of education and training programmes, it is also important to enhance the instructional methods used. For example, experiential learning methods where students are encouraged to develop problem-solving strategies can help to prepare learners for jobs in the constantly evolving renewable energy sector, where independent knowledge-seeking will often be necessary.

Facilitating collaboration between government agencies on workforce development, industry and educational institutions will contribute to more co-ordinated skill-matching efforts. It is vital to consider how a just transition can respond to potential labour displacement in the existing energy sector workforce and re-skill or upskill appropriately.

Targeted measures to train, recruit and retain women and other underrepresented or marginalised groups (including older workers, ethnic and religious minorities, people with disabilities and those on a low income) will ensure the dividends of the transition are enjoyed by all. This inclusion can be implemented through early exposure to renewable energy leadership and career pathways, targeted scholarships, government-funded training opportunities, and industry apprenticeship and mentorship schemes.

Outside the renewables industry, it is equally important to ensure sufficiently skilled and trained workers are available in government departments concerned with international trade, supply chains, electric charging infrastructure and land use. Fostering a broader understanding in the public sector of the interconnected nature of the energy transition, and the cascade effect of decarbonisation opportunities brought by a ramp-up of renewable electricity, can help to avoid knowledge silos and create more co-ordinated policy across different pillars of government.

Carefully designed public-private partnerships (PPPs) can also play a crucial role in improving overall training quality while meeting sectoral labour requirements, promoting national skill standards and matchmaking communities with workplace training opportunities. In addition to improving training content, PPPs can also play a role in shifting the financing of training provisions to a more integrated approach that incorporates multiple funding mechanisms including payroll-based training levies, tax incentives, scholarships and donations, vouchers and student loans (Dunbar, 2013).

URGENT RECOMMENDATIONS FOR POLICY MAKERS

- Align workforce planning among all stakeholders, including labour agencies, labour unions, the wider energy industry and educational institutions, to identify critical skill gaps and workforce needs in advance, and to design skill-building strategies accordingly.

- Provide capacity-building opportunities to a broad range of public sector departments – from energy to transport and industry – to foster a more comprehensive policy and technical understanding of different elements of the energy transition.

- Ensure energy transition goals are reflected in educational programmes and resources, such as university curricula, vocational training institutions, occupational health and safety training institutions, and professional education programmes.

- Build the talent pipeline by ensuring young people are exposed to renewable energy and transition career opportunities early in their education; and foster increased participation of women in the energy sector workforce.

- Invest in reskilling and upskilling measures for vulnerable communities and those in fossil fuel industries to ensure the employment benefits of the transition are extended to a wide subset of the population. Such measures need to be embedded in broader regional economic revitalisation programmes and investments.

SCALING-UP PUBLIC AND PRIVATE FINANCE 8